How a Brutal Court Ruling Exposed Washington’s Tax Crisis

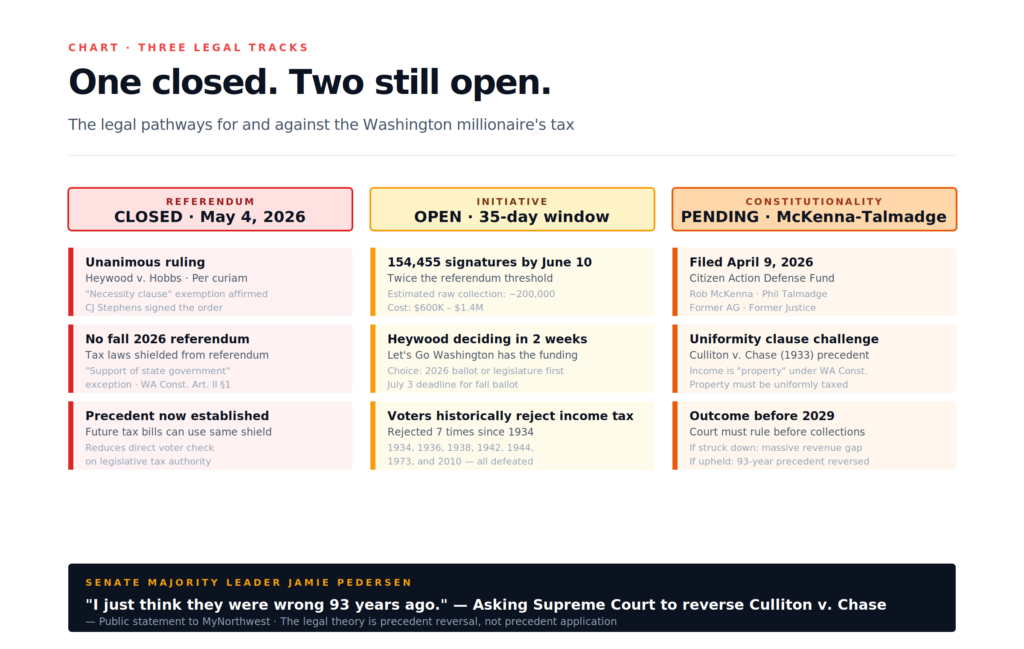

The Washington Supreme Court unanimously ruled on May 4, 2026 that voters cannot block the new Washington millionaire’s tax through a referendum. Specifically, the court found that Engrossed Substitute Senate Bill 6346 is shielded from referendum because Democratic lawmakers attached a “necessity clause” declaring the tax essential to state government operations. The 9.9% tax on household incomes above $1 million takes effect in 2028 with first payments due April 2029. Furthermore, Moody’s Investors Service flagged this exact legal vulnerability in their April 23 outlook downgrade. Opponents now face a steeper path: an initiative requiring 154,455 signatures by June 10 to qualify for the November ballot. A separate lawsuit challenging the tax’s underlying constitutionality, led by former Attorney General Rob McKenna and former Justice Phil Talmadge, is still pending. The fiscal pillar Moody’s flagged remains legally vulnerable. Here is what the ruling actually means.

What the Washington Millionaire’s Tax Ruling Actually Says

The Washington millionaire’s tax ruling came as a unanimous per curiam order from the state’s highest court. Specifically, the case is Heywood v. Hobbs — Brian Heywood and Let’s Go Washington against Secretary of State Steve Hobbs. Furthermore, the ruling resolves only the referendum question. It does not address the tax’s underlying constitutionality.

The Court’s Core Finding

Chief Justice Debra Stephens signed the decision. The key language from the order:

“ESSB 6346 undisputedly generates revenue for the state’s existing institutions and hence is similarly subject to the ‘support of state government’ exception to the referendum power.”

Specifically, the court ruled that the Washington Constitution’s Article II, Section 1 carves out tax-and-revenue measures from the referendum process. Furthermore, Stephens noted the order is “consistent with the words of the constitution and our unbroken line of precedent.”

In plain English: tax laws that fund state government cannot be referendumed. That precedent goes back over a century. Therefore, the legal question was not close.

Why the Necessity Clause Matters

Democratic lawmakers anticipated the referendum challenge. Specifically, they inserted language in ESSB 6346 declaring that the tax “is necessary for the support of the state government and its existing public institutions.” That declaration triggers the referendum exemption.

Furthermore, Secretary of State Steve Hobbs cited this clause when he initially rejected Let’s Go Washington’s referendum filing. The Supreme Court has now affirmed that rejection. Therefore, the necessity clause functioned exactly as the legislature designed it to function — as a statutory shield against referendum.

That is not new legislative practice. However, opponents argued the necessity claim was facially false because the tax does not begin generating revenue until 2029. Specifically, Heywood’s attorney Joel Ard argued in court filings that the legislature’s “necessity” declaration “negated any honest claim” that the bill was necessary for current state operations.

The court rejected that argument. Specifically, the order clarified that the constitutional exemption applies whenever a measure generates revenue for state institutions — regardless of when collections actually begin.

What This Did Not Decide

The court was explicit: this ruling does not address the constitutionality of the Washington millionaire’s tax itself. Specifically, the court order stated the case “did not address the constitutionality of the tax itself, but only whether the law could be subject to a referendum.”

Therefore, the broader fight continues. Furthermore, that broader fight is where the real legal risk lives.

How the Washington Millionaire’s Tax Got Here

The Washington millionaire’s tax did not appear out of nowhere. Specifically, it represents the third major attempt by state Democrats to introduce graduated income taxation in Washington over the past 15 years.

The Underlying Tax

Engrossed Substitute Senate Bill 6346 imposes a 9.9% personal income tax on household wage income above $1 million. Specifically:

- The first $1 million of income is exempt from the tax

- Tax applies only to income above that threshold

- The law takes effect in 2028

- First payments are due in April 2029

- Funds are designated for K-12 education, health care, human services, and higher education

Therefore, the tax structure is graduated by design — it applies only to households at the top of the income distribution. Furthermore, that structure is what makes it constitutionally vulnerable under Washington’s uniformity clause.

The 1933 Precedent Problem

In 1933, the Washington Supreme Court struck down a graduated income tax in Culliton v. Chase. Specifically, the court ruled that income is “property” under the state constitution, and therefore subject to the uniformity clause that requires all property to be taxed at the same rate. Furthermore, voters have rejected income tax measures seven times since then.

That is the precedent former Attorney General Rob McKenna and former Supreme Court Justice Phil Talmadge are challenging. Specifically, their lawsuit — filed April 9, 2026, on behalf of the Citizen Action Defense Fund — argues that ESSB 6346 violates the uniformity clause for the same reasons the 1933 court identified.

The Pedersen Argument

Senate Majority Leader Jamie Pedersen has been explicit about the strategy. Specifically, he is asking the court to reverse 93 years of precedent. From his comments to MyNorthwest:

“I am asking for the Supreme Court in 2026 — 93 years later — to take a second look at that, and we know that the Supreme Court all the time, both our Supreme Court and the U.S. Supreme Court, changes its mind periodically and has a new understanding. That’s all that’s going on, I just think they were wrong 93 years ago.”

Therefore, the legal theory of the case is not that the Washington millionaire’s tax fits within existing precedent. Specifically, the legal theory is that the existing precedent should be overturned. That is a much harder legal lift than fitting within precedent.

Why It Took 93 Years to Try Again

Income tax measures have been on Washington ballots in 1934, 1936, 1938, 1942, 1944, 1973, and 2010. Voters rejected each one. Therefore, the legislature has historically been the only realistic path to imposing graduated income taxation. Specifically, the 2026 legislative push represents the political coalition for the tax finally being strong enough to pass it through Olympia — even though voters have consistently rejected it at the ballot box.

That history matters for understanding why opponents are so focused on the referendum and initiative routes. Specifically: when voters get a direct say, they vote no. Therefore, the legislative-only path requires preventing voters from getting a direct say. The necessity clause inserted in ESSB 6346 is exactly that mechanism.

How the Washington Millionaire’s Tax Ruling Connects to the Moody’s Downgrade

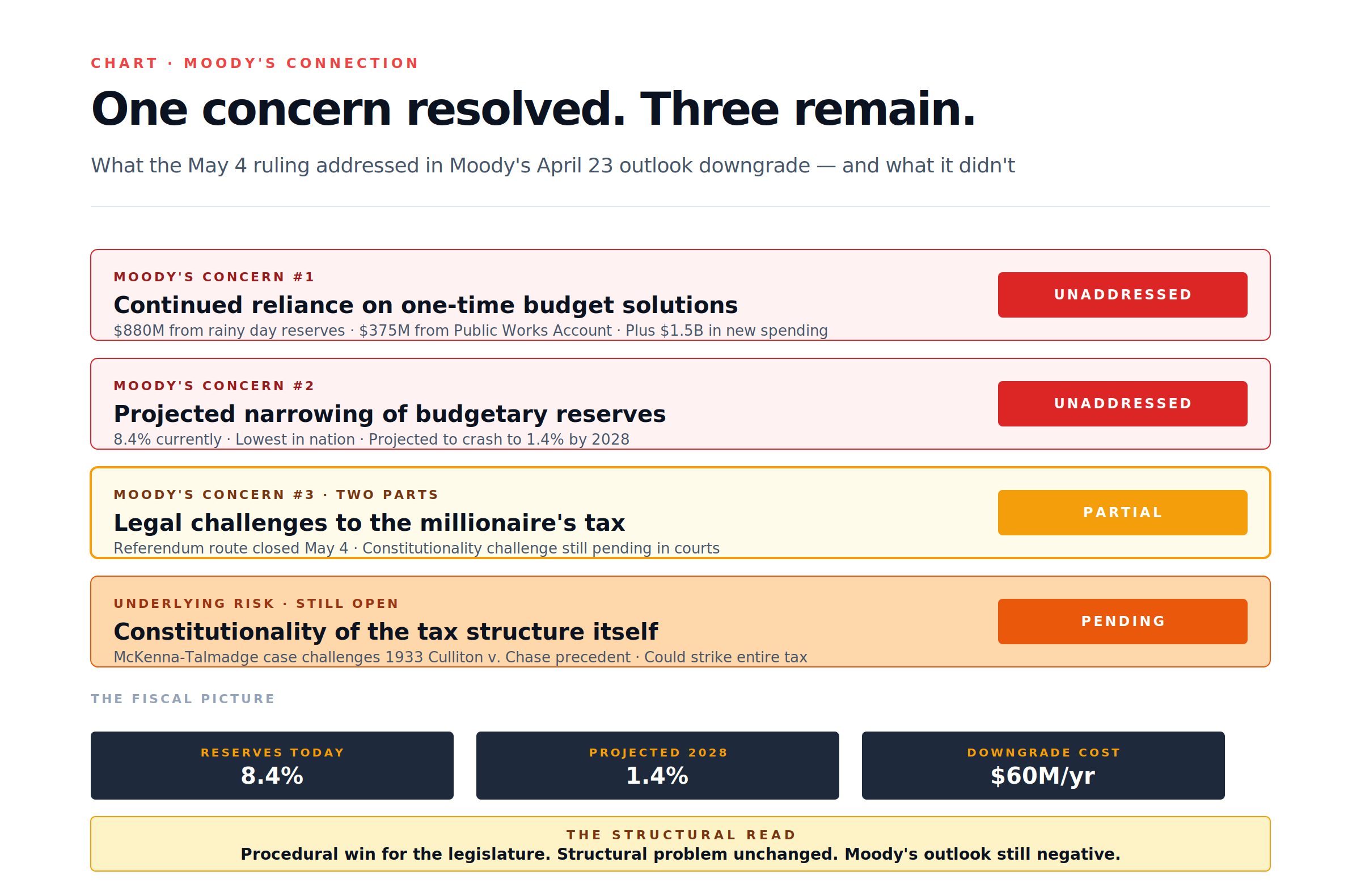

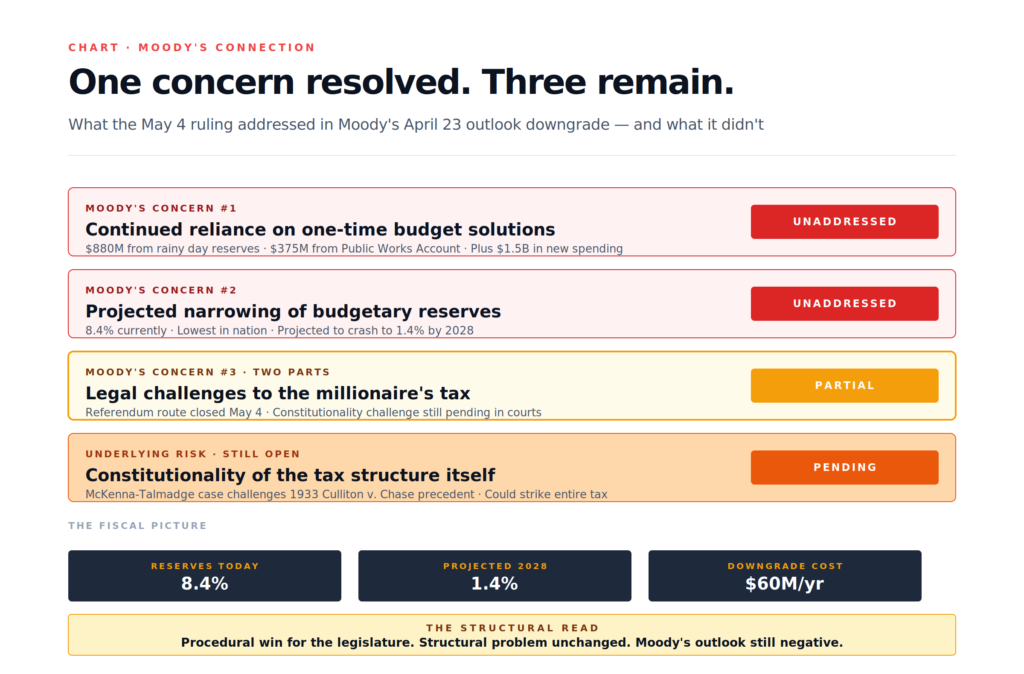

The Washington millionaire’s tax ruling matters most because of what it does — and does not — do for the state’s fiscal posture. Specifically, it confirms one part of what Moody’s flagged in their April 23 outlook downgrade. Furthermore, it leaves the larger risk unresolved.

What Moody’s Said in April

PNW Independent’s Moody’s Downgrade investigation documented the rating agency’s three concerns:

- Continued reliance on one-time budget solutions

- Projected narrowing of budgetary reserves

- Ongoing legal challenges to new revenues — specifically the millionaire’s tax

Therefore, Moody’s identified the Washington millionaire’s tax as a fiscal pillar. Furthermore, Moody’s flagged the legal challenges to that pillar as a specific concern. The April 23 ruling resolves part of the legal challenge — specifically, the referendum route is closed.

What the Ruling Resolves

The May 4 ruling provides the state with three concrete benefits:

- No fall 2026 referendum. The tax is not on the November ballot through the referendum process.

- Necessity clause precedent. Future tax measures can use the same shielding mechanism.

- Bond market reassurance. One vector of legal risk is closed.

Furthermore, House Majority Leader Joe Fitzgibbon characterized the ruling as expected: “It’s still good news for what we did this session and tax reform in Washington.”

What the Ruling Does Not Resolve

The ruling does not resolve the larger legal risk. Specifically, the McKenna-Talmadge constitutionality lawsuit is still pending. Furthermore, that lawsuit goes to the underlying validity of the tax structure — not just the procedural question of whether it can be referendumed.

If the court ultimately upholds the tax on constitutionality grounds, the fiscal pillar holds. However, if the court reverses the Culliton v. Chase precedent and strikes the tax down, the entire fiscal foundation Moody’s flagged collapses simultaneously.

That is the actual stakes. Specifically, the Washington millionaire’s tax is generating expected revenue starting 2028. Furthermore, that expected revenue is baked into the state’s biennial budget projections. Therefore, if the constitutionality challenge succeeds, Washington faces a sudden, multi-billion-dollar revenue gap with no replacement source identified.

The Moody’s Implication

Moody’s gave Washington a 12-to-18-month window to address structural problems. The May 4 ruling closes one risk vector. Furthermore, it does not address the others Moody’s flagged:

- Continued one-time budget solutions — unaddressed

- Reserves narrowing — unaddressed (8.4% currently, projected 1.4% by 2028)

- Constitutionality of the tax — still in litigation

Therefore, the ruling is good news for the state. Specifically, it is not sufficient news to remove the Moody’s outlook concern. The credit rating agency is watching the structural picture, not just one legal vector.

What State Officials Are Saying About the Washington Millionaire’s Tax Ruling

The political reaction broke along predictable lines. However, the language across statements reveals the broader strategic landscape.

Heywood: “Removing Any Guardrails”

Brian Heywood, founder of Let’s Go Washington and the principal funder of the referendum campaign, framed the ruling as a constitutional crisis. Specifically:

“This ruling states that the people cannot challenge via referendum any tax imposed by the legislature, removing any guardrails from the people on runaway spending.”

Furthermore, Heywood criticized what he characterized as the court’s selective use of precedent. Specifically:

“As they have relied so heavily on precedent in this ruling, for this court to be consistent, they should be expected to rely on precedent to reject the unconstitutional income tax as well. The income tax has 93 years of precedent and has been affirmed seven times. Not only have voters rejected it every time it’s been on the ballot, but our own court system has ruled it to be out of line with state law.”

That argument matters strategically. Specifically, Heywood is positioning the McKenna-Talmadge constitutionality lawsuit as a precedent-respecting challenge against a precedent-ignoring tax. Furthermore, Heywood is signaling that opponents will pivot to attacking the court itself if the constitutional challenge fails.

Heywood’s Court-Reshape Pivot

Five Washington Supreme Court seats are on the November 2026 ballot. Furthermore, Heywood argued the race now matters more than almost anything else on the November ballot:

“Shifting the ideological bent of this court, I think, is crucial for this state or the progressives in Olympia are just going to run roughshod straight over the Constitution, like Jamie Pedersen and Bob Ferguson are trying to do.”

Therefore, opponents are now pursuing three parallel tracks:

- Initiative to repeal the tax (July 3 deadline for 2026 ballot)

- Constitutionality lawsuit through McKenna-Talmadge

- Court reshape through November Supreme Court elections

That three-track strategy is significantly more expensive and time-consuming than the original referendum path. Specifically, an initiative requires twice as many signatures as a referendum — 154,455 by June 10.

Pedersen and Fitzgibbon: Vindicated

The Democratic legislators who designed the necessity clause approach were vindicated by the ruling. Specifically, Pedersen’s response acknowledged the court’s reasoning:

“The court upheld the plain language of the Washington constitution: tax measures are not subject to referendum challenges. As we have said all along, the proper way to challenge the Millionaires Tax is through the initiative process.”

Furthermore, Fitzgibbon characterized the outcome as expected: “But it’s still good news for what we did this session and tax reform in Washington.”

That framing is important. Specifically, the necessity clause was a deliberate strategic choice, not an oversight. Furthermore, Democratic lawmakers knew the legal precedent supported their position. Therefore, the May 4 ruling validates the strategic design — but it does not validate the underlying tax.

The McKenna Position

Former Attorney General Rob McKenna, who is leading the constitutionality lawsuit, has been blunt about the larger fight. Specifically, McKenna told KIRO Newsradio:

“This lawsuit that we brought to overturn this income tax and uphold the constitution is not just about a millionaires’ tax, or this particular bill, this test case, which the legislature has succeeded in creating, is about their ability to create any income tax that they want.”

Therefore, McKenna is framing the constitutionality challenge as an existential question for Washington’s tax system — not a single-tax dispute. Furthermore, that framing suggests the case is being prepared for the broadest possible legal review, not narrow technical arguments.

What the Initiative Path Requires

With the referendum route closed, opponents of the Washington millionaire’s tax must now use the initiative process. Furthermore, the initiative path is significantly more demanding than the referendum path.

The Numbers

To qualify an initiative for the November 2026 ballot, opponents need:

- 154,455 valid voter signatures by June 10, 2026

- That figure represents twice the threshold of a referendum (which would have required roughly 77,000)

- Furthermore, signatures typically have a 20-30% invalidation rate, meaning organizers need to collect approximately 200,000 raw signatures

- Cost estimate per signature: $3 to $7 depending on professional vs. volunteer collection

- Therefore, total signature gathering cost: roughly $600,000 to $1.4 million

That funding requirement is consequential. Specifically, only a small number of political committees can mobilize that capital on a 35-day timeline. Furthermore, Heywood’s Let’s Go Washington has the funding to pursue it but has not yet committed.

The Two-Week Decision Window

Heywood told Seattle Red 770 AM that a decision on whether to proceed will come within the next two weeks. Specifically, the choice is whether to push for the 2026 ballot (deadline July 3) or to go to the legislature first through Initiative to the Legislature. Furthermore, both options have strategic tradeoffs.

If Let’s Go Washington commits to the 2026 ballot, the campaign will need to mobilize within a four-to-six-week window. Therefore, the decision in the next two weeks effectively determines whether the Washington millionaire’s tax faces voter scrutiny in November or is delayed to a future cycle.

What the Washington Millionaire’s Tax Ruling Means for State Spending

The Washington millionaire’s tax ruling has implications beyond the immediate legal question. Specifically, it affects how the state can structure future revenue legislation. Furthermore, it has implications for Moody’s continued evaluation.

The Necessity Clause Precedent Now Established

Going forward, the Washington legislature can use the necessity clause to shield any tax measure from referendum. Specifically, this changes the political dynamic of revenue debates. Furthermore, opponents must now plan to use the initiative process for any tax they want voters to weigh in on directly.

That shifts the cost-benefit calculation for both sides. For the legislature, the necessity clause provides a procedural defense against referendum challenges. For opponents, every tax fight now requires initiative-level resources and timeline.

The Bond Market Read

Bond markets typically respond to reduced legal uncertainty positively. Specifically, the May 4 ruling removes one vector of risk from the Washington fiscal picture. Furthermore, it does so in a way that confirms the state’s procedural design held up under direct legal challenge.

However, Moody’s flagged three concerns in the April 23 outlook downgrade. The ruling addresses only one. Specifically, the reserves question and the one-time budget solutions concern are unaffected by the ruling. Furthermore, the constitutionality challenge still represents an existential risk to the new revenue stream Moody’s was implicitly counting on.

Therefore, the ruling is helpful but not sufficient. Specifically, Washington’s path back to a stable Aaa outlook still requires structural budget reform, not just legal wins on tax mechanics.

The Spending Implication

If the Washington millionaire’s tax holds through both the constitutionality challenge and any initiative campaign, the state has a stable revenue stream beginning 2029. Specifically, the projected revenue is meaningful — though exact figures depend on income distributions and behavioral responses.

However, if the tax is struck down on constitutionality grounds, Washington must immediately identify alternative revenue or absorb the loss through reserve drawdowns. Furthermore, the state’s reserves are already projected to crash to 1.4% by 2028 even with the tax revenue assumed. Therefore, losing the tax revenue would push reserves below operational minimums.

That scenario is exactly what Moody’s flagged. Specifically, the rating agency was not concerned about the tax existing — it was concerned about the legal vulnerability of the tax. The May 4 ruling addresses one vector of that vulnerability. The constitutionality challenge remains.

What Should Happen Next on the Washington Millionaire’s Tax

The Washington millionaire’s tax ruling closes one chapter and opens several others. Specifically, here is what should happen next.

1. Constitutionality Case Should Move Quickly

The McKenna-Talmadge lawsuit was filed April 9, 2026. Furthermore, the case will eventually need a Supreme Court ruling to provide finality. Therefore, the courts should expedite the constitutionality review to provide certainty before tax collections begin in 2029. Specifically, every additional month of legal uncertainty preserves the fiscal risk Moody’s flagged.

2. Legislature Should Prepare a Backup Revenue Plan

Prudent fiscal management requires planning for the contingency that the tax is struck down. Specifically, the legislature should identify backup revenue sources that could be activated if the constitutionality challenge succeeds. Furthermore, those backup sources should be statutorily ready, not just theoretically discussed. Hope is not a fiscal strategy.

3. The Reserves Issue Still Needs Direct Action

The May 4 ruling does not address Washington’s reserves problem. Specifically, reserves are at 8.4% — the lowest of any U.S. state — and projected to fall to 1.4% by 2028. Furthermore, the legislature should establish a statutory reserve floor of at least 10% to prevent further drawdowns. The Washington millionaire’s tax may eventually generate revenue, but reserves are an operational concern that exists independent of any future revenue stream.

4. The November Court Election Deserves Public Attention

Five Washington Supreme Court seats are on the November ballot. Furthermore, Heywood is now positioning the court reshape as the path to defeating the tax through the constitutionality challenge. Therefore, Washington voters should evaluate the candidates on their judicial philosophy, not just on their stance on any single case. Specifically, the court will rule on issues far beyond this one tax.

5. Transparency on Tax Revenue Projections

The Washington millionaire’s tax is projected to generate revenue. However, the specific projections vary significantly based on behavioral assumptions. Specifically, if high earners restructure income, relocate, or reduce taxable income, projected revenues fall. Furthermore, the legislature should publish detailed revenue scenarios — best case, base case, worst case — to support honest public debate about whether the tax delivers on its promises.

The Bottom Line on the Washington Millionaire’s Tax Ruling

The Washington millionaire’s tax ruling is a procedural victory for the legislature. Specifically, the necessity clause maneuver worked as designed. Furthermore, the unanimous Supreme Court order means the legal precedent supporting that maneuver is now firmly established for future tax debates.

However, the ruling does not resolve the larger fiscal picture. The constitutionality challenge remains. Reserves are still at the lowest level in the nation. The structural deficit that drove the Moody’s outlook downgrade is unaffected by the May 4 decision. Furthermore, the political backlash that produced the May Day rallies and Mayor Wilson’s “bye” remark to wealthy residents continues to define the political landscape going into the November election.

Therefore, the ruling matters less for what it changes than for what it confirms. Specifically: Washington’s fiscal future depends on a contested 9.9% tax that voters cannot referendum, that opponents are still trying to strike down on constitutional grounds, and that produces no revenue until 2029. That is the reality Moody’s was flagging in April. The May 4 ruling does not change it.

For Washington taxpayers, the practical question is now simpler. If the constitutionality challenge succeeds, the state is in a sudden multi-billion-dollar revenue hole with reserves at the lowest level of any state. If the challenge fails, the state collects the revenue but the underlying structural deficit remains. Furthermore, the November court election will substantially affect which scenario unfolds.

The ruling closes the referendum route. The fight continues on every other front. The clock is running on initiative signatures, the constitutionality lawsuit, and the November ballot. Each of these will determine whether the Washington millionaire’s tax actually delivers what its supporters promised — or whether the legal architecture surrounding it collapses on contact with serious challenge.

The math has not changed. Washington still needs the revenue. Washington still has the lowest reserves in America. The Moody’s outlook downgrade is still active. And the constitutionality of the underlying tax is still an open question. The May 4 ruling resolves one piece of that puzzle. The rest remains very much in play.

Related Reading on PNW Independent

- Moody’s Downgrade: Washington State Built This Hole

- FEMA Denial: Washington Loses $36.6M for Future Floods

- KCRHA Audit: $13M Missing in Seattle’s Homeless Agency

- Who Really Runs Seattle: Two Machines, One Ruling Class

External Sources

- Washington State Standard — WA Supreme Court bats down referendum attempt targeting income tax (May 4, 2026)

- MyNorthwest — Washington Supreme Court blocks referendum on millionaires’ tax (May 4, 2026)

- FOX 13 Seattle — WA Supreme Court blocks voter referendum on millionaires tax

- KOMO News — Washington Supreme Court blocks challenge on new ‘millionaires tax,’ citing constitution

- Cascadia Daily News — State Supreme Court nixes quick referendum to repeal new ‘millionaires tax’

- The Center Square via Columbia Basin Herald — WA Supreme Court blocks bid to put state income tax before voters

- Seattle Red — WA Supreme Court Kills Income Tax Referendum (Jason Rantz Show)

- Lynnwood Times — WA Supreme Court rules “Necessity Clause” shields new income tax law from voter referendum

- Washington State Legislature — ESSB 6346